On Tuesday evening, the value of one bitcoin shot above $10,000. It has been a remarkable run for a currency that was only worth about $12 five years ago.

The run has been particularly remarkable because it's still not clear what Bitcoin is useful for. During its early years, the cryptocurrency garnered a lot of optimistictalk about how it would disrupt conventional payment networks like MasterCard or Western Union. But almost nine years after Bitcoin was created, there's little sign of it becoming a mainstream technology. Few people own any bitcoins at all. Even fewer use it as a daily payment technology.

Yet that hasn't prevented the cryptocurrency's value from zooming upward. One factor driving Bitcoin's growth has been the emergence of a broader cryptocurrency ecosystem. Bitcoin serves as the reserve currency for the Bitcoin economy in much the same way that the dollar serves as the main anchor currency for international trade.

In this piece, we'll explain the key innovation that set Bitcoin apart from all previous electronic payment schemes. We'll look at how Bitcoin won over regulators and venture capitalists to become a significant part of the global financial system. And we'll examine the cryptocurrency boom of the last year that has helped drive Bitcoin's value into the stratosphere.

While we can tell the story of Bitcoin's rise and point to some of the factors that have pushed its value upward, we can't really explain why the currency's value goes up or down during a particular day, week, or month. In particular, bitcoins have more than doubled in value since the start of October, which is hard to explain with anything other than speculative mania. People thinking about trying to get in on the Bitcoin boom should think carefully about the potential downside and not invest any money they can't afford to lose.

Bitcoin was the first truly decentralized electronic payment network

Cypherpunks have dreamed of fully decentralized electronic payment systems for decades. The potential for cryptographically secure electronic money became obvious after the invention of digital signatures using public-key cryptography in the 1970s.

But efforts to create practical digital cash schemes were bedeviled by something called the double-spending problem: how to prevent someone from sending the same digital coins to two different people. Preventing this requires a shared ledger that records all transactions. And until 2008, no one had figured out a way to do this without relying on a central authority to maintain and update the ledger.

Then someone calling himself Satoshi Nakamoto proposed an approach that initially seemed a little crazy: just have everyone on a peer-to-peer network keep a copy of every transaction, forever. Obviously, that's not the most efficient way to design a payment network, but a transaction doesn't need to take up very much space—and bandwidth and storage space get cheaper every year.

The key to Nakamoto's scheme was a clever, fully decentralized way to reach a consensus about the order of transactions within the blockchain, Bitcoin's transaction ledger.

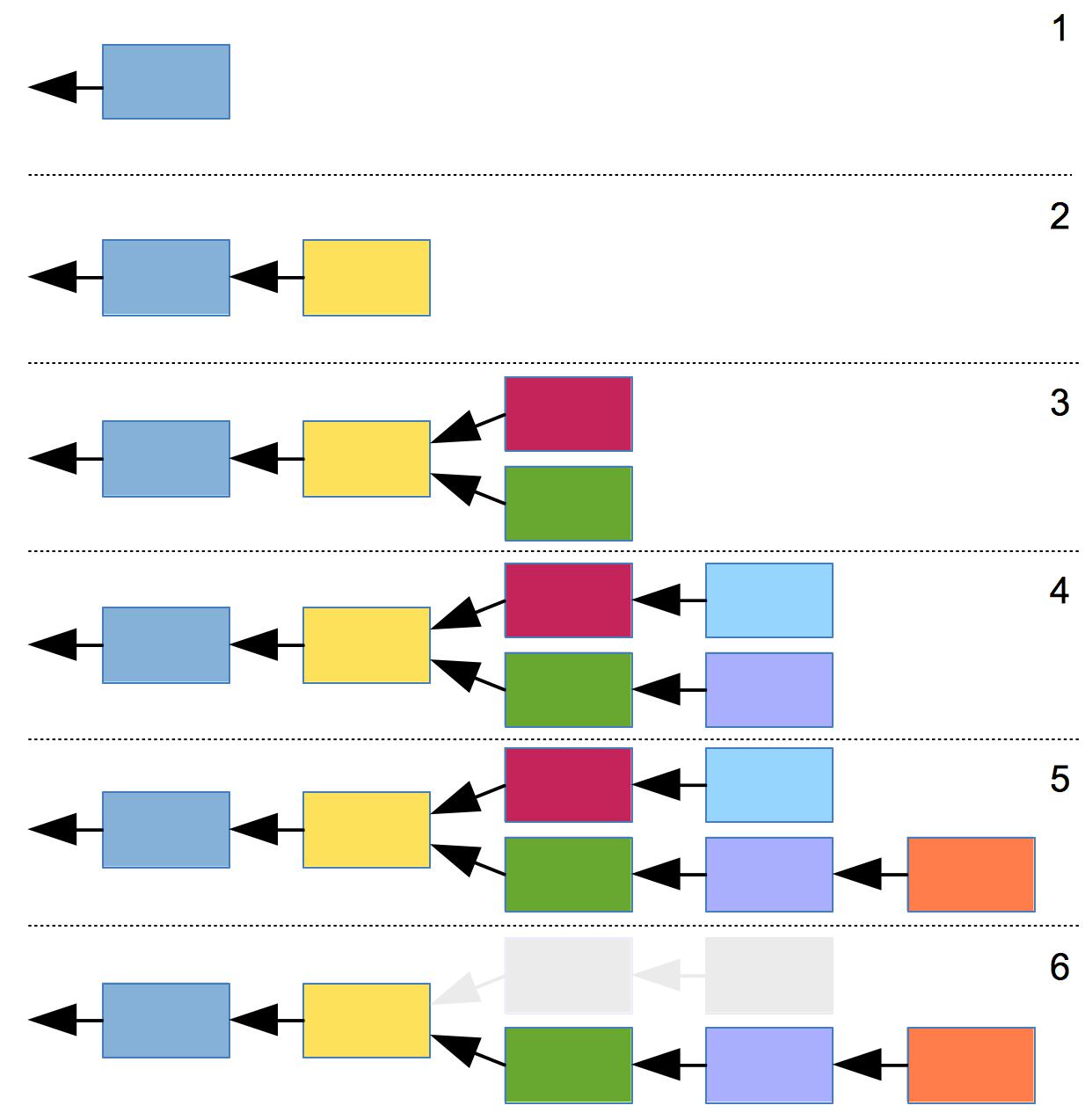

Certain nodes on Bitcoin's peer-to-peer network, known as miners, compete for the right to add the next block to the Bitcoin blockchain. Using brute force, they race to find a block whose SHA-256 hash value is below an arbitrary threshold (known as the difficulty). Once a node finds a block that meets the criteria, it announces the new block to other nodes on the network. Others incorporate the new block into their copy of the blockchain and then begin the race anew.

Occasionally, two miners discover blocks close enough together that the network doesn't agree about who was first. Only one block can be accepted by the network. But which one? The network decides by moving on to the next round of the race. Every miner starts looking for a second new block building on one of the two rival blocks in the previous round. When someone finds a new block, it will include a hash value pointing back to one of the previous blocks. Once this happens, both the newly discovered block and the preceding block its creator chose become part of the official blockchain. The other, competing block gets discarded.

In theory, this could happen multiple times—two nodes could discover blocks simultaneously in the second round, deepening uncertainty about which chain is the legitimate one. But if nodes are being honest, this situation won't last for long.

Nodes are programmed to always build on top of the longest chain—on the block with the largest number of predecessors. So as soon as someone discovers a block that makes its chain longer than other, rival chains, everyone else has a financial incentive to abandon other chains and work from the longest one. In the image above, nodes will abandon the red and light-blue blocks as soon as the orange block is announced in step five, making the green and violet blocks into consensus picks.

Everyone has an incentive to always work from the current longest block because the creator of a block gets to award itself a fixed number of newly created bitcoins—currently 12.5 bitcoins per block. But this reward only becomes official if the block becomes part of the consensus blockchain. If a miner tries to build on a block further back in the chain, any new block they discover won't be on the longest chain. The miner, therefore, won't get a reward.

Bitcoin charms Washington

In the early months of 2011, Satoshi Nakamoto gradually became less involved in the Bitcoin project. He turned over official leadership of the project to developer Gavin Andresen and disappeared from public view. Bitcoin had gained enough momentum to continue without him.

Bitcoin started getting mainstream attention in 2011, and much of it wasn't positive. One of the earliest applications of Bitcoin was for a website called Silk Road, a Tor hidden service that operated as a kind of eBay for illegal drugs. The existence of Silk Road came to the attention of Sen. Chuck Schumer (D-N.Y.), one of the first elected officials to comment on the technology. And he wasn't happy.

Silk Road, he said, "represents the most brazen attempt to peddle drugs online that we have ever seen." Bitcoin, in Schumer's view, was "an online form of money laundering used to disguise the source of money."

It's easy to imagine things continuing like that, with federal officials moving to shut down the Bitcoin network the same way they'd shut down previous electronic money schemes that had been too accommodating of illicit transactions. But savvy lobbying by Bitcoin insiders and their supporters in the libertarian think-tank world convinced officials to take another path.

These supporters pointed out that shutting down Bitcoin altogether would likely prove impossible. Banning it in the US would merely push it overseas. And if Bitcoin activity was centered in a jurisdiction hostile to the United States, then law enforcement would lose the power to subpoena Bitcoin companies that might have valuable information about illicit uses of the Bitcoin network.

Meanwhile, advocates argued that Bitcoin had the potential to be a major new source of technological innovation.

Over the course of 2013, law enforcement officials and members of Congress became convinced of these arguments. The Senate's first hearings on Bitcoin, held in November 2013, turned out to be Bitcoin lovefests, with the nation's top money-laundering official emphasizing that "innovation is a very important part of our economy."

On Tuesday evening, the value of one bitcoin shot above $10,000. It has been a remarkable run for a currency that was only worth about $12 five years ago.

The run has been particularly remarkable because it's still not clear what Bitcoin is useful for. During its early years, the cryptocurrency garnered a lot of optimistictalk about how it would disrupt conventional payment networks like MasterCard or Western Union. But almost nine years after Bitcoin was created, there's little sign of it becoming a mainstream technology. Few people own any bitcoins at all. Even fewer use it as a daily payment technology.

Yet that hasn't prevented the cryptocurrency's value from zooming upward. One factor driving Bitcoin's growth has been the emergence of a broader cryptocurrency ecosystem. Bitcoin serves as the reserve currency for the Bitcoin economy in much the same way that the dollar serves as the main anchor currency for international trade.

In this piece, we'll explain the key innovation that set Bitcoin apart from all previous electronic payment schemes. We'll look at how Bitcoin won over regulators and venture capitalists to become a significant part of the global financial system. And we'll examine the cryptocurrency boom of the last year that has helped drive Bitcoin's value into the stratosphere.

While we can tell the story of Bitcoin's rise and point to some of the factors that have pushed its value upward, we can't really explain why the currency's value goes up or down during a particular day, week, or month. In particular, bitcoins have more than doubled in value since the start of October, which is hard to explain with anything other than speculative mania. People thinking about trying to get in on the Bitcoin boom should think carefully about the potential downside and not invest any money they can't afford to lose.

Bitcoin was the first truly decentralized electronic payment network

Cypherpunks have dreamed of fully decentralized electronic payment systems for decades. The potential for cryptographically secure electronic money became obvious after the invention of digital signatures using public-key cryptography in the 1970s.

But efforts to create practical digital cash schemes were bedeviled by something called the double-spending problem: how to prevent someone from sending the same digital coins to two different people. Preventing this requires a shared ledger that records all transactions. And until 2008, no one had figured out a way to do this without relying on a central authority to maintain and update the ledger.

Then someone calling himself Satoshi Nakamoto proposed an approach that initially seemed a little crazy: just have everyone on a peer-to-peer network keep a copy of every transaction, forever. Obviously, that's not the most efficient way to design a payment network, but a transaction doesn't need to take up very much space—and bandwidth and storage space get cheaper every year.

The key to Nakamoto's scheme was a clever, fully decentralized way to reach a consensus about the order of transactions within the blockchain, Bitcoin's transaction ledger.

Certain nodes on Bitcoin's peer-to-peer network, known as miners, compete for the right to add the next block to the Bitcoin blockchain. Using brute force, they race to find a block whose SHA-256 hash value is below an arbitrary threshold (known as the difficulty). Once a node finds a block that meets the criteria, it announces the new block to other nodes on the network. Others incorporate the new block into their copy of the blockchain and then begin the race anew.

Occasionally, two miners discover blocks close enough together that the network doesn't agree about who was first. Only one block can be accepted by the network. But which one? The network decides by moving on to the next round of the race. Every miner starts looking for a second new block building on one of the two rival blocks in the previous round. When someone finds a new block, it will include a hash value pointing back to one of the previous blocks. Once this happens, both the newly discovered block and the preceding block its creator chose become part of the official blockchain. The other, competing block gets discarded.

In theory, this could happen multiple times—two nodes could discover blocks simultaneously in the second round, deepening uncertainty about which chain is the legitimate one. But if nodes are being honest, this situation won't last for long.

Nodes are programmed to always build on top of the longest chain—on the block with the largest number of predecessors. So as soon as someone discovers a block that makes its chain longer than other, rival chains, everyone else has a financial incentive to abandon other chains and work from the longest one. In the image above, nodes will abandon the red and light-blue blocks as soon as the orange block is announced in step five, making the green and violet blocks into consensus picks.

Everyone has an incentive to always work from the current longest block because the creator of a block gets to award itself a fixed number of newly created bitcoins—currently 12.5 bitcoins per block. But this reward only becomes official if the block becomes part of the consensus blockchain. If a miner tries to build on a block further back in the chain, any new block they discover won't be on the longest chain. The miner, therefore, won't get a reward.

Bitcoin charms Washington

In the early months of 2011, Satoshi Nakamoto gradually became less involved in the Bitcoin project. He turned over official leadership of the project to developer Gavin Andresen and disappeared from public view. Bitcoin had gained enough momentum to continue without him.

Bitcoin started getting mainstream attention in 2011, and much of it wasn't positive. One of the earliest applications of Bitcoin was for a website called Silk Road, a Tor hidden service that operated as a kind of eBay for illegal drugs. The existence of Silk Road came to the attention of Sen. Chuck Schumer (D-N.Y.), one of the first elected officials to comment on the technology. And he wasn't happy.

Silk Road, he said, "represents the most brazen attempt to peddle drugs online that we have ever seen." Bitcoin, in Schumer's view, was "an online form of money laundering used to disguise the source of money."

It's easy to imagine things continuing like that, with federal officials moving to shut down the Bitcoin network the same way they'd shut down previous electronic money schemes that had been too accommodating of illicit transactions. But savvy lobbying by Bitcoin insiders and their supporters in the libertarian think-tank world convinced officials to take another path.

These supporters pointed out that shutting down Bitcoin altogether would likely prove impossible. Banning it in the US would merely push it overseas. And if Bitcoin activity was centered in a jurisdiction hostile to the United States, then law enforcement would lose the power to subpoena Bitcoin companies that might have valuable information about illicit uses of the Bitcoin network.

Meanwhile, advocates argued that Bitcoin had the potential to be a major new source of technological innovation.

Over the course of 2013, law enforcement officials and members of Congress became convinced of these arguments. The Senate's first hearings on Bitcoin, held in November 2013, turned out to be Bitcoin lovefests, with the nation's top money-laundering official emphasizing that "innovation is a very important part of our economy."